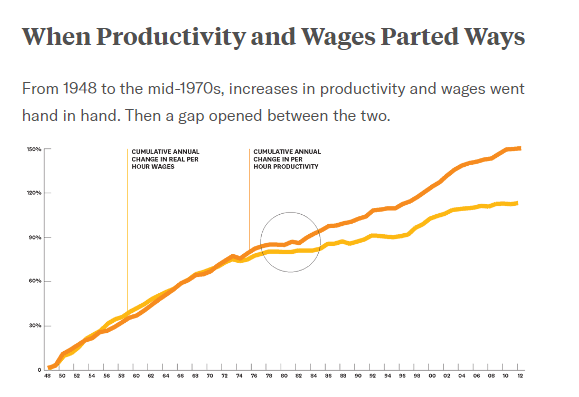

While American workers are increasing their productivity, the companies that pay them are not rewarding their productivity with commensurate pay increases, and this has been the case for the past half-century. Prior to the mid-1970s, rises in productivity and pay were entwined and rose together at the same level, but we have been leaving workers behind since then.

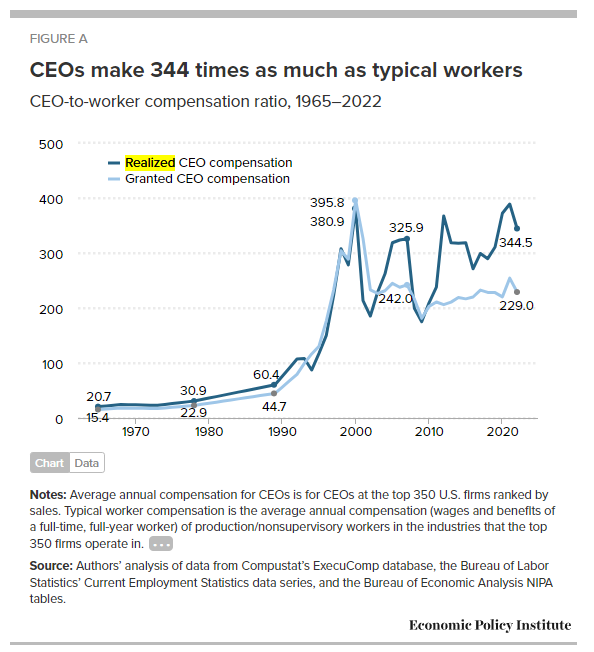

And a huge part of the reason for this is the skyrocketing level of CEO and executive pay, especially relative to worker pay. Depending on how you look at stock options, average CEO to average worker pay at the top 350 companies by sales was at a ratio of 15-21 to 1 in 1965; by 1989, this had risen to about 44-60 to 1, and by 1995 this had jumped to about 117-131 to 1, then about 381-396 to 1 in 2000, adjusting by 2021 to 254-389 to 1 (the higher numbers on the ranges reflect stock options that are realized over time after they are granted, the lower numbers in the set the values when they are granted). Currently, U.S. CEO pay is an extreme outlier among other developed economies in absolute terms and in terms of the CEO to worker pay ratio.

There is no reason why we should tolerate this. We can still be the most creative and dynamic economy in the world, we can still reward entrepreneurs and visionaries with massive wealth, but we can also impose reasonable limits to make the economy work more for the masses of American workers who truly form the backbone of the economy.

Therefore, I propose a series of new regulations and changes to the tax code that will help generate more wealth for working-class Americans without stifling economic growth, especially as our economy was the envy of the world even more so in earlier decades without the extreme imbalance of CEO compensation we see today.

CEO-to-Worker Pay Gap

For all medium-sized businesses and larger (500 or more employees as defined by the U.S. Small Business Administration) and small business making $60 million or more in profit, companies that pay their CEOs:

- In excess of 100 times more than the average non-executive worker salary at its own company would pay an additional 5% tax on the amount paid to all executives in addition to existing taxes

- In excess of 150 times, a 10% tax on executive pay

- In excess of 200 times, a 15% tax on executive pay

- In excess of 250 times, a 25% tax on executive pay

- In excess of 300 times, a 35% tax on executive pay

- In excess of 350 times, a 50% tax on executive pay

- In excess of 400 times, a 65% tax on executive pay

Taxes on stock options that are part of executive compensation would be assessed when they are realized, as opposed to granted. All these would be paid by the company as part of corporate taxes due, not by the individual executives and CEOs.

Tax Breaks for Paying Employees More

Also for all the same businesses:

- All pay of non-executive workers that are at least 30% of the average non-executive workers pay can have 50% of the portion of that worker pay that is above 30% of the average up to 65% of the average salary deducted from the taxes the company owes

- For at least 65% of the average pay, 75% of pay that is at least 65% of average pay up to the average pay can be deducted

- For at least average or higher pay, 100% of pay that is at least average up to $100,000 can be deducted

Fairness for Tipped Workers

Finally, the federal minimum wage exemptions for tipped workers would be eliminated so that all workers would be paid the minimum wage before any tips are considered.

Now is the time to raise my candidacy to be an integral part of this race, now is the time to spread the word, now is the time to donate to my campaign, now is the time to really get things going.

Oh, and there’s a debate this morning, 11AM in Frederick!